أعمال موجهة في مقياس الهندسة المالية (السداسي الثاني)- للأستاذ بدروني عيسى- السنة الدراسية: 2023/2024

Aperçu des sections

-

-

Forum

-

على الطلبة الكرام (كل طالب منفردا) أن يضمن الأعمال التالية:

1- إنجاز البحوث.

2- ترجمة النصوص من الإنجليزية إلى العربية بشكل مختصر.

-

-

-

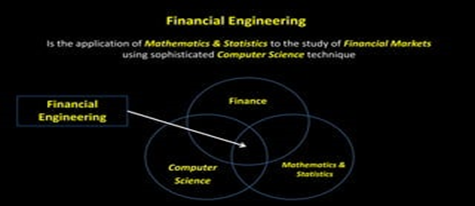

Financial Engineering

We see modern Financial Engineering as the science of data-driven decision making in business environments. Building more accurate models reduces uncertainty around future events and paths the way to better decision making. It is a mix of broad decision-making applications, sound data and modeling work, paired with an entrepreneurial drive to solve innovation challenges using modern software and financial thinking, that makes Financial Engineering a unique experience.

1. Meaning Of Financial Engineering

Financial engineering involves the utilization of mathematical techniques in solving financial problems. This process uses tools and knowledge forme the fields of economics, statistics, applied mathematics, and computer science. These tools assist in solving the prevailing financial issues and help in devising innovative financial products. Financial engineering is also known as quantitative analysis. Basically, it is a corporate restructuring strategy. Investment banks, commercial banks, and insurance agencies use this technique.

2. Financial engineers

Financial engineers create, design, and implement new financial models and processes to find solutions for problems. They always seek new financial opportunities. Preparing such models requires a great deal of research, and they rely on in-depth data analysis, simulations, risk analysis, and stochastics. Financial engineers possess knowledge in fields such as economics, statistics, and corporate finance. These engineers work in banking, consulting agencies, securities, and financial management.

3. Factors Influencing Financial Engineering

The following are the factors that influence the growth process of financial engineering :

3.1. Environmental Factors

These are the factors that exist in the external environment. Environmental factors have a direct impact on the firm.

These factors are not controllable. Political, Economic, Social, and Technological (PEST) analysis can be conducted to determine these factors and their impact on the business. Common environmental factors are technological advancements, new inventions, competitiveness, and political and economic changes.

3.2. Intra Firm Factors

The firm controls these factors and directly affects the financial engineering process. Examples of intra-firm factors are accounting policies, risk aversion, agency costs, and liquidity needs.

4. Example

An example of financial engineering in practice is the work of quantitative analysts – usually referred to as “quants” – who develop things such as algorithmic or artificial intelligence trading programs that are used in the financial markets.

For example, some scholars believe that over-reliance on financial models has, in some instances, created, rather than solved, financial problems. Following the 2008 Global Financial Crisis, some economists blamed the banks’ widespread use of the Black-Scholes formula – a popular mathematical model used for investing in financial derivative instruments – for precipitating, or at least contributing to, the severity of the worldwide economic crash.

Financial Engineering in Practical Business Applications:

The use of financial engineering was key to facilitating a sale by Amoco Corporation of its subsidiary, MW Petroleum Corporation, to the Apache Corporation in the early 1990s. The factor that became the ultimate sticking point for concluding a deal was the two companies’ divergent opinions on the likely future prices of oil and gas – Amoco was bullish, and Apache was bearish.

A bit of financial engineering led to the creation of a financial product referred to as a capped price support warranty that was offered by Amoco to Apache. The warranty provided that in the event of oil prices dipping below a designated level, Amoco would make supporting payments to Apache to reduce its losses in revenue.

In return for receiving the warranty, Apache promised, in turn, to make additional payments to Amoco in the event that, in the first few years following the sale of MW Petroleum, oil prices rose above a designated level. Both the lower and upper designated price levels were determined by financial engineers using financial models.

In such a case, financial engineering provided a means for the two companies involved in the transaction to share the considerable risks in the uncertain environment of major commodity prices in a manner that was acceptable to both parties and that, thereby, made it possible for them to conclude the deal for Apache’s acquisition of MW Petroleum.

5. Uses of Financial Engineering

Financial engineering is used across a broad range of tasks in the financial world. Some of the areas where it is most commonly applied are the following:

Corporate Finance

Arbitrage Trading

Technology and Algorithmic Finance

Risk Management and Analytics

Pricing of Options and other Financial Derivatives

Behavioral Finance

Creation of Structured Financial Products and Customized Financial Instruments

Quantitative Portfolio Management

Credit Risk and Credit Management

Conclusion

Financial engineering can benefit organizations in finding solutions to various problems such as risk management, scenario simulation, and new product development. However, owing to the ever-increasing financial innovation, there is a perpetual demand for highly skilled financial engineers.

-

-

-

Types of Derivatives Instruments

Derivatives Instruments

A derivative is a financial instrument that derives its value from an underlying asset. The underlying security could be shares, bonds, currencies, commodities, and more. These financial instruments are relatively intricate tools that many may find hard to comprehend but they offer hefty rewards as well. Investors or traders primarily use these instruments for hedging and speculation purposes.

Similar to shares, investors can trade derivatives contracts as well. Some derivatives contracts trade over-the-counter (OTC), while some trade on recognized exchanges. Some of the biggest derivatives exchanges in the world are the CME Group, Eurex, and the Korea Exchange. There are mainly four types of derivatives. Let us know about them in detail.

Table of Contents

1. Types of Derivatives

1. Forward Contract

2. Futures

3. Options

4. Swaps

2. Final Words

Types of Derivatives

Following are the types of derivatives:

Forward Contract

Forward contracts are the oldest and simplest types of derivatives. In this, the buyer or the holder of the forward contract enters into an agreement to buy the underlying asset at a specific price and date in the future. Such types of contracts give holders more flexibility than any other types of derivatives. This is because such contracts do not trade on recognized exchanges and are highly customizable, thus, provide traders with the flexibility to customize the price and expiry date of contracts. Such type of derivatives trades in the over-the-counter market, and thus, it is a direct contract between two parties.

Since there is no involvement of exchange, these contracts carry higher counterparty credit risk. The terms of the forward contracts remain as decided between the two parties, who may or may not make it public. We also call such contracts ‘forward commitment’ because the parties do not get the right to cancel the contract.

Also Read: Derivatives Market – Types, Features, Participants and More

Suppose Mr. A owns a car and plans to sell it a year later. But he is of the view that the value of his car will decrease after one year due to regular wear and tear. So he goes to the second-hand car dealer and sell second-hand cars and shares his thought regarding the uncertainty of the price he will receive after a year for his car. The dealer put forward an idea to enter into a forward contract today where he (the dealer) will buy Mr. A’s car a year later at a price they agree on today.

Futures

The working modalities of future contracts are like that of a forward contract. Similar to the forward contracts, these agreements are also an obligation for the parties. The only difference between the two is that futures are standardized contracts that trade on established exchanges. Thus, the parties to a futures contract can not tailor the contractual points. Also, unlike the forward contracts, the buyer and seller do not enter into a contract with each other directly. Instead, they enter into a contract with the exchange. Moreover, all such contracts and their terms and conditions are no more private, as it is in the contracts of the exchange-traded market.

Futures contracts have a fixed format, size, and expiration. As all these contracts are traded on the exchange, they follow the exchange’s standard daily settlement process. This means the losses and gains settle on a daily basis. Such procedures help to reduce counterparty credit risk.

For example, Mr. A expects the price of Company X shares to go up in the near future. Thus, Mr. A buys Company X futures at the current price. Now, if the price of shares goes up in the future, Mr. A would still be able to buy shares of Company X at less than the market price.

Options

These are the most popular types of derivatives. Unlike forward and futures contracts, options give the holder a right. But he is under no obligation to exercise his right to buy or sell the underlying asset at a specific rate and date. In case of an option, the right is only available to the buyer. For the seller, however, options are an obligation. It means that the seller would have to fulfill the contract if the buyer exercises the option.

Options have two variants – the call option and the put option. The call options give the holder the right (not obligation) to acquire the underlying asset at a future date and at a specific price. The opposite is the status of a put option. Thus, the put option holder has the right (not obligation) to sell an underlying asset at a future date and at a specific price.

So, we can say that investors have 4 choices for trading options. They can be:

Buyers of a call option.

Buyers of a put option.

Sellers of the call option.

Sellers of the put option.

The buyer of the option has to pay a charge or fee, and we call it the option premium. Also, there are three different types of options on the basis of exercisation – European, American, and Bermudan. Depending on the type (European, American, and Bermudan), the holder can exercise the option on or before the expiry.

Assume Company A expects shares of XYZ to gain next month. Company A does not own the shares of XYX, whose current price is $10. Thus, Company A buys call options worth $2, which gives it the right to purchase shares of XYZ on or before the expiry. Now assume that the share price rose to $12. Company A will now use the option to buy the shares, which are worth $12, at $10. It means a profit of $2 per share, excluding option costs.

In both – the call and put – option, the seller must fulfill the contract if the buyer wants.

Swaps

Swaps are the most intricate derivative tools. These derivatives allow parties to exchange or swap cash flows. Most swaps involve the exchange of fixed cash flow for a floating cash flow. Similar to other types of derivatives, swaps can be of commodity, currency, interest rate, or more. Interest rate swaps are the most common types of swaps.

For example, Company ABC has a loan of $10,000 at a variable interest rate of 10%. Company ABC, however, is worried that the interest rate may rise significantly in the future. Thus, it enters into a swap agreement with Company XYZ, which is ready to exchange the 10% variable rate with a 12% fixed rate.

Now, Company ABC will pay interest at 12% to Company XYZ, who, in turn, would pay interest at 10% to the lender. In reality, the parties pay only the difference amount, in this case, 2%.

Swaps, generally, do not trade on any exchange. They are private agreements where two parties negotiate directly with each other. Thus swaps do carry a high amount of credit risk. Swaps are also risky because, ‘interest and currency’ – its most popular underlying assets – are volatile.

Final Words

All types of derivatives are a good investment avenue for experienced investors to put their surplus funds. They have emerged as popular tools to either hedge risk or make money by speculating. However, they are risky, as well. Investors must fully understand derivatives markets and instruments, as well as their consequences.

-

-

-

Leçon

Forward Contract

Forward Contracts

A forward contract is the most elementary form of derivatives. Over here, two parties enter into an agreement either to buy or sell something at a future date agreed today. It can be customized to cater to the need of both parties entering into the contract. The contract specifies the underlying asset’s contract size or a lot, forward interest rate, settlement date, specified quality, and quantity, and other items to be fulfilled to satisfy the contract.

The assets often traded in forward contracts include commodities, precious metals, electricity, oil, natural gas, foreign currencies, and financial instruments.

Table of Contents

1. Forward Contracts

2. Pricing Assumptions for Forward Contract

3. Closing a Position

4. Settlement for Forward Contract

1. Cash

2. Physical Delivery

5. Purpose

6. Value

7. Merits of Forward Contract

8. Demerits of Forward Contract

Pricing Assumptions for Forward Contract

The following assumptions are used to compute forward prices:

1. There are no transaction costs.

2. No restriction on short sales.

3. There are the same tax rates on all net profits.

4. Borrowing and lending at the risk-free rate

5. Arbitrage opportunities are exploited as they arise.

Closing a Position

In contrast to a futures trade, where a buyer or seller performs an opposite transaction of their original transaction to close a position, for a forward contract to be closed or terminated before the settlement date, there are two ways to do so. Either transfer the contract to a third party or get into a new forward contract with the opposite trade. It is typically complicated to terminate a contract and might attract a penalty. (Read more about Forwards vs Futures).

Settlement for Forward Contract

Forwards can be settled in either of two ways:

Cash

It requires the counterparties to exchange the cash difference in the value of their positions. The appropriate party receives the cash difference.

Physical Delivery

It requires the counterparties to exchange the underlying asset. Herein, the actual quantity of the underlying asset, along with other specifications as stipulated in the contract, are delivered to settle the contract.

After a settlement, there are no further obligations to either party.

Purpose

Generally, forwards are used to hedge/mitigate the price movement risk by locking the price today for the transaction to occur at a future date.

Value

The initial value of a forward contract is zero. The forward contract can possess a non-zero value only after the contract is entered into and the obligation to buy or sell has been made. Since the forward price is regularly computed to prevent arbitrage, the value must be zero at the inception of the contract.

Merits of Forward Contract

A forward contract has the following merits:

1. They are easy to understand.

2. It is a tailor-made contract and is flexible to adjust to the needs of both parties.

3. Offer a complete hedge (i.e., delta neutral hedge) and helps in mitigating the risk.

4. It can be matched with the time period and cash flows of exposure.

5. As it is an over-the-counter (OTC) contract, the price of contracts is not known to others, hence providing price protection.

6. There are no immediate cash outflows before the settlement of the contract but might require an upfront fee, i.e., margin.

7. It is a tool for speculation.

8. Payoffs are symmetrical, meaning thereby, there is a distinction as one party will gain while the other makes a loss of an equivalent amount.

9. There is no daily marking to market requirements as mandatory in the futures contract.

Demerits of Forward Contract

Like every other derivative, forwards also have some demerits as follows:

1. As it is a private contract, there is no liquidity.

2. Counterparty risk of defaulting on the contract is excessively high.

3. The market of forward contracts is extremely unorganized as it is traded over the counter.

4. It may be challenging to find a counterparty to enter into a contract.

Bas du formulaire

Types of Forward Contracts – All You Need to Know

A forward contract is a type of derivative instrument. This is an agreement between two investing parties wherein the parties agree to buy or sell an underlying asset or security at a future date at an agreed rate in the agreed quantity. These contracts trade OTC (over the counter), and thus they do not face many regulations and are not standardized. There are many types of forward contracts, which we will discuss later in this article.

Traders primarily use forward contracts to protect themselves from the volatility in the currency and commodity markets. But, forward contracts can involve other assets as well, including equity, treasury, real estate, and more. Forward contracts are useful as a hedging instrument. However, it is also used by investors for speculation purposes to earn profits from the movement of the security prices.

Table of Contents

1. Types of Forward Contracts

1. Window Forwards

2. Long-Dated Forwards

3. Non-Deliverable Forwards (NDFs)

4. Flexible Forward

5. Closed Outright Forward

6. Fixed Date Forward Contracts

7. Option Forward Contract

2. Final Words

3. Frequently Asked Questions (FAQs)

Now, as we know what forward contracts are, let us take a look at the types of forward contracts.

Types of Forward Contracts

Since currencies account for the bulk of forward contracts, most types of forward contracts are specific to currencies. Following are the types of forward contracts:

Window Forwards

Such forward contracts allow investors to buy the currencies within a range of settlement dates. Basically, such contracts allow investors to get a more favorable and convenient exchange rate than what they would get by using a standard forward contract.

Also Read: Forward Contract

For example, Mr. X is supposed to make a settlement with his US-based supplier after three months. However, the date is not fixed. Therefore, Mr. X opts for a window forward contract where he can trade on any day from 1st to 30th of the upcoming 4th month but not later than 30th.

Long-Dated Forwards

As the name suggests, the settlement period of such contracts is much more than the usual forward contracts. A standard forward contract usually has an expiry date of up to 12 months. In contrast, long-dated forwards can have a maturity date of up to 10 yrs. Except for a longer settlement date, all other features of long-dated forwards are the same as standard forward contracts.

Non-Deliverable Forwards (NDFs)

Non-deliverable forwards are types of forward contracts that are very different from standard forward contracts. As in such contracts, physical delivery of the security/asset of funds does not occur. Instead, the parties just exchange the difference amount at the time of the settlement. The difference amount is on the basis of the contract rate and the market rate at the time of the settlement. Generally, investors who do not have enough funds or do not want to commit funds or block huge funds go for such types of forward contracts.

Suppose XYZ Inc. will receive 1 million BRL after 3 months for sales made in the current month. It goes to a Brazilian bank in order to enter into a forward contract of selling 1 million BRL after 3 months at a rate of 4 BRL for $1.

Also Read: Non-deliverable forward (NDF)

Now, there are 2 possibilities:

Case 1: After 3 months, $1 = 3.7 BRL, or

Case 2: After 3 months, $1 = 4.25 BRL.

XYZ Inc. would receive $250,000 for sure because of entering into an NDF contract.

In case 1, amount to be received by XYZ Inc. = $270,270 (1 million BRL / 3.7). Here, the spot price turns favorable for XYZ Inc. Now the Brazilian bank will pay the difference of the spot rate and forward rate to XYZ Inc., which is $20,270 (i.e., 270,270 – 250,000).

In case 2, amount to be received = $235,294 (1 million BRL / 4.25) which is less than $250,000. Here, spot price is unfavorable for XYZ Inc. Now the difference paid by the bank is $14,706 (i.e., 250,000 – 235,294).

Flexible Forward

Such type of forward contract gives investors flexibility in exchanging the funds. Or, we can say that investors using such a contract have an option to exchange the funds before the settlement date. Using this contact, parties can either exchange the funds outright or choose to make several payments prior to the settlement date.

Assume that Mr. X imports goods in India worth $500,000 from a US-based exporter. Being aware of exchange rate fluctuation, he enters into a flexible forward contract. This will help him to make payments at different points of time during the period of the contract, whenever the exchange rates are favorable to him.

Closed Outright Forward

This is the simplest type of forward contract. We can also call such forward contracts European contracts or Standard Forward Contracts. Such types of contracts allow investors to exchange the underlying asset at a specific future date.

Say, for example, you have entered into a trade with a foreign exporter. And, the date of payment is the 24th of next month. You can lock in the exchange rate by entering into a closed outright forward contract for the 24th of next month.

Fixed Date Forward Contracts

In this type of forward contract, the parties exchange the underlying asset only at specific maturity date. Or, we can say, such contracts have a fixed maturity date. Most forward contracts are fixed-date forward contracts only.

Option Forward Contract

These types of forward contracts are similar to flexible forward contracts. An option forward contract allows parties to exchange the underlying security on any date during a specific

period.

Final Words

So, these were the types of forward contracts that investors have at their disposal. They can select one or more forward contracts depending on their position, risk appetite, as well as the current market scenario.

-

-

-

على الطلبة الكرام تلخيص الكتاب المرفق في حدود 5 صفحات فقط

-

-